Consumer and Worker Protection311Search all NYC.gov websites

Consumer and Worker Protection311Search all NYC.gov websites

Tuesday, September 29, 2015

Abigail Lootens

Department of Consumer Affairs

(212) 436-0042

press@dca.nyc.gov

Stu Kantor

Urban Institute

(202) 261-5283

skantor@urban.org

NYC Department of Consumer Affairs Releases New Reports: 1.14 Million Households in NYC are Unbanked or Underbanked; More Than Half of New Yorkers Don't Have Adequate Savings for an Emergency

NEW YORK, NY—Department of Consumer Affairs (DCA) Commissioner Julie Menin today announced the results of two new studies—Where Are the Unbanked and Underbanked in New York City? and How Do New Yorkers Perceive Their Financial Security?—that look at New Yorkers’ use of banks and their perception of financial security. The research shows that in 2013, 11.7 percent of households in New York City (360,000 households) did not have bank accounts, surpassing the national figure of 7.7 percent. An additional 780,000 households, or one in four, were underbanked meaning they had a bank account but also used alternative financial services. Between 2011 and 2013, the number of households without a bank account decreased but the number of underbanked households increased. Additionally, more than half of New Yorkers reported that they didn’t have enough savings to weather an emergency and one in three reported having too much debt. To better understand New Yorkers’ use of banks and sense of financial health and develop more effective future programming and products, DCA’s Office of Financial Empowerment (OFE) commissioned the Urban Institute to conduct the studies and develop the accompanying interactive map depicting the data. It is the first effort to capture and compare the unbanked, underbanked, and levels of perceived financial security in New York City’s 55 neighborhoods.

“DCA’s Office of Financial Empowerment is dedicated to educating and empowering New Yorkers to replace financial hardship with financial stability,” said DCA Commissioner Julie Menin. “Having and using a bank account helps families save money and guard against unexpected financial emergencies—a security that more than half of New Yorkers do not have. The findings of these reports will serve as a driving force behind our future work as we create targeted programs for key neighborhoods and build towards a more equitable city, a cornerstone of Mayor de Blasio’s OneNYC.”

“Disasters like Hurricane Sandy capture our attention, but everyday emergencies, such as unexpected bills or a health crisis, leave many families unprepared and exposed. Programs that help families build savings can provide financial protection and stability,” said Caroline Ratcliffe, a senior fellow at the Urban Institute and the study’s lead author.

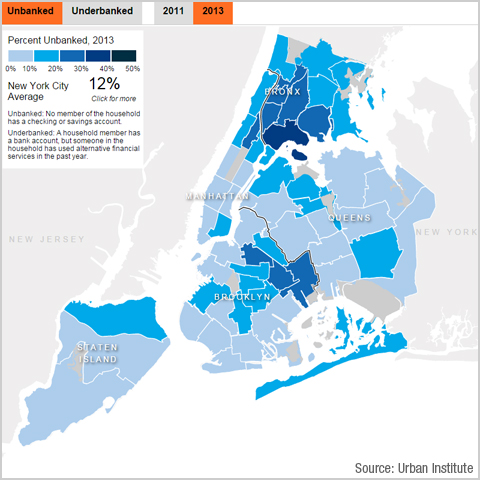

Percent of Unbanked Households in New York City, 2013

Key findings from Where Are the Unbanked and Underbanked in New York City? and How Do New Yorkers Perceive Their Financial Security? include:

New Yorkers are more likely to be unbanked and underbanked than the rest of the country.

- 360,000 households in New York City do not have bank accounts;

- an additional 780,000 households in New York City are underbanked, meaning they have a bank account but continue to use alternative financial services, like check cashers, nonbank money orders, prepaid cards, remittances, and pawnshops;

- 11.7 percent of New York City households are unbanked compared to 7.7 percent of U.S. households and 25.1 percent are underbanked compared with 20 percent of U.S. households;

- compared to New York City as a whole, Bronx households are more than twice as likely to be unbanked, with 21.8 percent reporting that they do not have a bank account. One third (30.5 percent) of the households in the borough are underbanked; and

- Staten Island has the lowest number of unbanked households (7.2 percent) and the lowest number of underbanked households (18.8 percent).

Between 2011 and 2013, the number of households without bank accounts decreased but the number of underbanked households increased.

- following the national trend (8.2 percent in 2011 to 7.7 percent in 2013), the unbanked rate in New York City fell from 14.3 percent in 2011 to 11.7 percent in 2013. There were declines in four of the five boroughs: Bronx, Brooklyn, Manhattan, and Queens. The borough with the lowest unbanked rate—Staten Island—remained steady at seven percent;

- between 2011 and 2013, the share of underbanked households in New York City increased from 22.4 percent to 25.1 percent, offsetting the decline in the unbanked rate. Three of the five boroughs (Bronx, Brooklyn, and Manhattan) experienced a decrease in the share of households without a bank account and an increase in the share of households with a bank account that also use alternative financial services.

In addition to having inadequate savings and too much debt, one in three New Yorkers express dissatisfaction with their personal finances, which is similar to the national rates.

- three out of five New Yorkers (57.5 percent) report not having enough savings to cover three months of expenses in the case of an emergency (58.4 percent nationally);

- one out of three New Yorkers (28.8 percent) perceive they have too much debt (30.2 percent nationally);

- one out of three New Yorkers (30 percent) express dissatisfaction with their personal finances (31.9 percent nationally);

- Bronx has the highest share of people who feel financially insecure—66.6 percent have inadequate emergency savings, 30.9 percent perceive they have too much debt, and 36.4 percent feel financially unsatisfied; and

- Staten Island has the lowest share—45.8 percent, 26.3 percent, and 22.3 percent, respectively.

DCA commissioned the Urban Institute, a Washington D.C.-based economic and social policy research organization, to analyze the usage of banks and the perception of financial security of New Yorkers on a neighborhood level. The studies analyze household data from the Federal Deposit Insurance Corporation’s (FDIC) 2011 and 2013 National Survey of Unbanked and Underbanked Households, the FINRA Investor Education Foundation’s 2012 National Financial Capability Study, and the United States Census Bureau’s American Community Survey, as well as qualitative interviews conducted for the agency by RTI International.

DCA will use these findings to continue to develop creative solutions to address financial insecurity and underlying related issues like the use of a bank account, lack of savings and debt. Some of these solutions include, a collaboration with the Mayor’s Fund to Advance New York City, that is currently reviewing proposals from organizations to identify solutions that will help improve the financial health of targeted communities. DCA is also creating a safe and transparent auto loan product to protect New Yorkers from predatory loans while buying a used car. Earlier this year, DCA launched an expanded public awareness and education campaign to inform New Yorkers of the City’s free tax preparation options and important tax credits, such as the Earned Income Tax Credit and the NYC Child Care Tax Credit. This resulted in a resounding 50 percent increase in New Yorkers who used the City’s free tax preparation services (totaling 150,000 individuals). The campaign successfully returned more than $250 million in tax refunds and savings to New Yorkers with low incomes.

DCA offers free one-on-one financial counseling at its network of Financial Empowerment Centers to help New Yorkers learn about managing their money, paying down debt, and opening a bank account. The City, in partnership with banks and credit unions, also offers the NYC SafeStart Account, a safe and affordable starter savings account for New Yorkers. The account features no overdraft fees or monthly fees (if a minimum balance is met), minimum balance requirements of $25 or less, and an ATM or debit card for withdrawals. DCA worked with participating institutions and 12 banks and credit unions now accept IDNYC as the primary form of identification to open an account.

For more information about DCA OFE’s work, to learn how to open a NYC Safe Start Account, or make an appointment at a Financial Empowerment Center, visit nyc.gov/consumers or call 311.

The Department of Consumer Affairs (DCA) licenses, inspects, and educates businesses, assists and informs consumers, mediates complaints, and offers free financial counseling and safe banking products. DCA enforces the Consumer Protection Law, the Paid Sick Leave Law and other related business laws throughout New York City and licenses nearly 80,000 businesses in 55 different industries. For more information, call 311 or visit DCA online at nyc.gov/consumers or on its social media sites, Twitter, Facebook, Instagram and YouTube.