Consumer and Worker Protection311Search all NYC.gov websites

Consumer and Worker Protection311Search all NYC.gov websites

News from the Independent Democratic Conference

FOR IMMEDIATE RELEASE

Thursday, April 30, 2015

Contact: Candice Giove 347.866.6742

FOR IMMEDIATE RELEASE

Thursday, April 30, 2015

Contact: Candice Giove 347.866.6742

Senators Klein & Savino Reveal Top Predatory Subprime Auto Lending Practices in New York

Investigative report proposes legislative remedies to tricky tactics, fraudulent practices and deceptive scams unscrupulous city car dealers are using to prey on financially vulnerable New Yorkers

Queens, NY — Independent Democratic Conference Leader State Senator Jeff Klein (D-Bronx/Westchester) and State Senator Diane Savino (D-Staten Island/Brooklyn) on Thursday released an investigative report, “Road to Credit Danger: Predatory Subprime Auto Lending in New York.” Senators Klein and Savino, joined by NYC Department of Consumer Affairs Commissioner Julie Menin, Queens District Attorney Auto Crime and Insurance Fraud Unit Chief ADA Mary Lowenburg, consumer attorneys and predatory subprime auto lending victims, exposed top tactics currently employed in predatory subprime auto lending.

Senators Klein and Savino unveiled a comprehensive package of 11 bills as part of their report to combat predatory subprime auto lending practices in New York State. Without government intervention, this largely ungoverned financial product poses a threat to the market akin to the 2008 subprime mortgage crisis.

“A New Yorker could have bad credit, no credit or hardly any income and still get a car loan. Let’s make no mistake, this is the subprime mortgage crisis reloaded. Lenders think that they could hoodwink us into believing that their bad behavior has stopped, but they’ve just shifted gears. Now lenders see that predatory subprime auto loans could be their next payday, but we in the New York State Senate are watching. We will pass legislation to get ahead of this practice before it becomes the next bubble to burst on the backs of hardworking New Yorkers,” said state Senator Klein.

“If it sounds too good to be true, it is. Using deceptive practices to get vulnerable New Yorkers to sign loans they could never afford to pay is unconscionable. As the Chair of the Senate’s Committee on Banks we will pass legislation to shield consumers from abusive lending practices before we wind up in a crisis similar to 2008,” said Senator Savino.

“We must pull the emergency brake and put a stop to these abusive practices, now. Reminiscent of the housing crisis from which we are finally starting to recover, auto loan lenders are now preying upon the most vulnerable individuals who they know full well are unable to repay their predatory loans. To take a play from lenders' own books, let's pull the kill switch on these deceptive practices and restore fairness for New Yorkers who are in the market to purchase both used and new vehicles,” said Senator Jose Peralta (D-Queens).

Unscrupulous dealers often appeal to consumers with bad credit, no credit or living on fixed incomes by offering guaranteed approval for financing through enticing online advertisements, the investigation found. Once at a dealership, unsophisticated or unsuspecting customers fail to realize loan applications contain abusively high interest rates, sky-high financing mark-ups, or are even sometimes filled in with fraudulent income information. In the end, consumers wind up with cars costing as much as twice the price on financing terms they could never afford to repay.

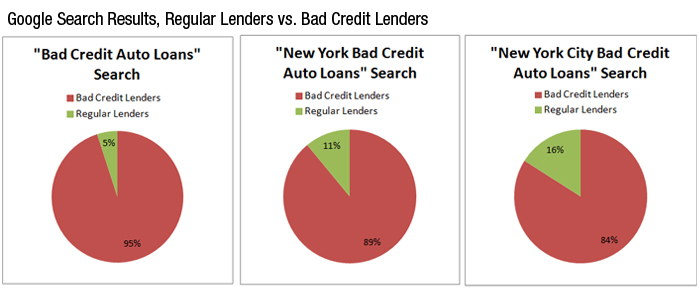

An analysis of Google search terms: “Bad Credit Auto Loans,” New York Bad Credit Auto Loans and “New York City Bad Credit Auto Loans” leads to hundreds of pages of lender sites offering subprime loans. It’s no wonder consumers with poor credit are lured to car dealerships that might engage in these practices because of bold online advertisements guaranteeing 100% approval, even for those with the worst credit circumstances.

The report also details popular ploys used in predatory subprime lending:

- Abusively high interest rates - Loans offered to individuals with poor credit contain sky-high interest rates that could hover around 24% and because these consumers are already the least likely to be able to pay off a loan, repossession rates are very high.

- Abusive loan to value ratio financing - With incredibly high interest rates built into subprime loans and pressure to purchase vehicle customizations that are rolled into the loan, a car buyer could wind up paying in excess of 200% of the original price of the vehicle.

- Dealer Financing Mark-Ups - Unbeknownst to many consumers dealers are legally allowed to mark-up interest rates on loans. No disclosure requirements exist.

- Dealership Fraud - Dealers often force buyers to purchase extras such as VIN-etching, service contracts, warranties, insurances and anti-theft measures in order to qualify for a loan and fail to tell them that none of these add-ons are necessary to obtain financing. The added cost is rolled into a loan that could have an interest rate as high as 24%.

- Fraudulent Loan Applications - Court cases illustrate instances where dealers fill in false income levels in order for a consumer to obtain a loan. Many consumers never see a loan application before it is submitted to a lender.

- Spot Delivery Scams - Dealerships allow consumers to drive away with a vehicle promising financing and later call to say that financing was denied and they must either accept the less desirable new terms or return the vehicle.

- GPS Tracking Devices - Cars financed through subprime loans often have GPS tracking devices so that cars can be located and repossed. This method of tracking is unregulated and consumers often don’t realize that they consented to this in a contract.

- Vehicle Kill Switches - This device shuts off a car remotely by the lender if a buyer doesn’t pay a loan on time.

For some victims of predatory subprime auto lending, a form of justice came from Queens District Attorney Richard A. Brown, whose investigators nabbed used car dealer Julio Estrada who defrauded auto consumers at a Northern Boulevard dealership. Mr. Estrada is now serving a two to four year sentence.

“In the guise of helping consumers achieve their dream of owning a vehicle of their own, some dealer finance representatives trick unwary vehicle purchasers into taking out loans that are far beyond their means. Often, the result is ruined credit for the purchaser and the repossession of the vehicle by the dealer. I thank Senators Klein and Savino for shining a light on this important issue and for standing up on behalf of all New Yorkers,” said Queens District Attorney Brown.

However, while criminal prosecution is a great first step in cases of illegal fraud, it does not make victims financially whole again. Even though Mr. Estrada faced criminal prosecution, for many of these victims, recovering financially has been difficult or impossible due to the current flawed structure of New York’s consumer protection laws and lenders’ limited liability under rules concerning assignees. The IDC’s package of reforms hopes to provide better avenues of civil recovery for all vulnerable consumers who are harmed by these practices so that they can continue on with their lives.

The City’s Department of Consumer Affairs (DCA) licenses used car dealerships and receives hundreds of complaints about the industry each year. DCA is currently investigating subprime auto lending, working to identify partners to create a safe and affordable auto loan product, and has advocated on a city and state level for increased regulation.

“Dealerships have been deceiving New Yorkers with impunity for far too long. We often hear about well-informed consumers who take smart steps to protect themselves, but nevertheless end up signing for ruinous loans that are much higher than they wanted or agreed to. Moreover, the banks that provide the financing do not take seriously complaints and other signs of fraud by the dealerships whose businesses they keep afloat. These unscrupulous practices have to end, and MFY applauds the NY Senate for taking on this issue,” said MFY Legal Services, Inc. attorney Ariana Lindermayer.

“A car is the most expensive purchase that most New York City families will ever make. That being the case, it is absolutely financially devastating to those families when they get ripped off in the car buying process. Whether the car turns out to be a "Lemon", has undisclosed accident damage, or if they are victimized by abusive lending and financing fraud the results for the typical family can be devastating,” said consumer attorney David Kasell.

In the wake of the 2008 subprime mortgage crisis, Senator Klein authored landmark foreclosure protection legislation, signed into law in late 2009, which put in place vital protections for thousands of New York homeowners in danger of losing their homes. In 2014, the laws were extended and kept in place the requirement for lenders to provide 90 days notice of foreclosure and mandatory settlement conferences for all home loans. However, the practice of subprime auto lending remains unregulated in the State of New York.

New York State could take action against predatory subprime auto lending, though the nationwide problem and much of the banking industry must be regulated federally. The IDC is proposing the following 11 bills to protect New York consumers:

- Usury Rate Reform - Many times auto dealerships are at the crux of the predatory subprime auto lending problem. Since dealerships act as the original lender, these businesses should be subject to the state usury rate, which is the maximum rate at which a lender could issue a loan. In New York that stands at 16%. This proposal caps the usury rate at 10% for used vehicle purchases over $7,000.

- Increase Lender Liability - Lenders are often complicit in fraudulent loan applications. This legislation would hold them jointly liable with an auto dealership. It would also authorize the New York State’s Department of Financial Services to develop regulations for auto loan applications, income verification and consumer complaints.

- Limit Dealer Mark-Up Discretion - Dealers can add-on anywhere from 0-3% to the financing APR of a vehicle without a consumer’s knowledge, and studies have found widespread racially discriminatory practices at play. This would require disclosure of a dealer mark-up at the time of sale, and would also request the Department of Financial Services to conduct a study on the issue of mark-ups to determine how dire this discrimination problem is, and how we can work to remedy it.

- Standardize and Increase Surety Bond Levels - Currently a used auto dealer only requires a $10,000 surety bond to do business, but often when they are held accountable for wronging a consumer they default. This legislation would increase used auto dealers required surety bonds to $100,000 to protect consumers because of the high risk nature of their business. New auto dealers surety bonds would remain at $50,000.

- Regulate Dealer Advertising - As discovered in the investigative report, dealers and subprime financiers often target customers with bad credit or no credit through internet advertisements promising a 100% approval rating. Many times these ads deceive those collecting SSI and SSD. This legislation would authorize the State’s Division of Consumer Protection to regulate used auto dealership advertising and ban dealerships from misrepresenting that SSI and SSD are sufficient income sources for loans.

- Transparency Reform - A uniform loan form for used car financing would be created by the State’s Department of Financial Services. This form would disclose all costs and warn consumers that add-on costs are not required to obtain loans and what the loan to value ratio is upon financing. This legislation would also ban all conditional deliveries.

- License Financial managers at Dealerships - The State’s Department of Financial Services would license all financial managers who provide loans to customers at auto dealerships, and would require all dealerships who issue financing or facilitate financing to designate and license a finance manager.

- Strengthen New York’s Unfair and Deceptive Acts and Practices (UDAP)-Style Statue - It’s hard for a consumer to sue a used car dealership in New York because of the high cost of litigation. This legislation allows for class action suits and also requires reasonable attorney’s fees to be paid to the plaintiff in a UDAP-style suit.

- Ban Vehicle Kill Switches - Kill switches are activated remotely and can pose serious safety risks to consumers. This would stop the use of kill switches throughout the state.

- Require a Cooling Off Period - Most major retail purchases provide a buyer with a window to cancel a transaction, but car purchases have no cooling off period. This would require a three-day cooling off period for used car purchases, giving consumers the opportunity to review lengthy financial documents and return a used automobile within three days. It would also create the same opportunity for new car transactions, although a car must remain in a lot for the duration of the cooling off period since a new vehicle automatically loses value as soon as it’s driven off a lot.

- Create a SONYMA-Style Auto Loan Program - A state loan program financing consumers with subprime credit would be created to help vulnerable customers obtain cars and repay loans at reasonable rates.